- by Rebecca Gray

- December 16, 2020

- Uncategorized business startup Superannuation tax

Is it the Right Time to Start a Business?

It’s clear, pandemics are a health crisis that also cause economic disaster. It would appear as though we are only seeing the tip of the iceberg with hundreds of thousands of businesses going into hibernation, collapsing and permanently closing. For the first time in three decades Australia is officially in recession with Victorians having been in an extended lockdown and subject to a curfew . But no State is in the clear as we saw recently with Adelaide experiencing a brief but hard lockdown.

It’s clear, pandemics are a health crisis that also cause economic disaster. It would appear as though we are only seeing the tip of the iceberg with hundreds of thousands of businesses going into hibernation, collapsing and permanently closing. For the first time in three decades Australia is officially in recession with Victorians having been in an extended lockdown and subject to a curfew . But no State is in the clear as we saw recently with Adelaide experiencing a brief but hard lockdown.

It has been described as a ‘perfect storm’ and we are sailing in uncharted waters. The media is flooding us with COVID-19 information and governments are using vocabulary that is normally reserved for war time. They are committing record amounts of money to assist business owners and employees but sadly, this recession spells financial doom for some businesses and industries including travel, events and entertainment are under threat. Given these facts and all the uncertainty, is it the right time to start a business?

Historically, business start-ups tend to surge when there are high levels of unemployment and middle management lose their jobs. Research also suggests that close to ten percent of the population are always planning to start a business. Our current circumstances are extreme but there’s never a perfect time to launch a business. At the moment people may be experiencing more focus and clarity regarding their priorities and vision. As such, provided you have done your homework that we touch on below, there is no reason to postpone your start-up plans.

If you’re in start-up mode, the most important advice we can offer you right now is, failing to plan is planning to fail. This serves as both advice and a warning because while it’s exciting when you have that light bulb moment and idea for a new business, starting (or buying) a business necessitates research, risk, passion and planning. While it’s hard not to get carried away with the excitement, starting a business is a process that can take months not days. There are very few shortcuts and no amount of enthusiasm, money, hard work or talent can guarantee business success.

Before You Pull The Business Trigger

If you’re thinking of quitting your job in favour of starting a business make sure you have done your homework. The Australian Bureau of Statistics reports that almost half of all new businesses close within three years of start-up. Make no mistake, the life of a new business owner can be a real roller coaster ride. The moment you transition from being an employee to being self-employed, your income is no longer guaranteed and you lose benefits like employer funded superannuation and 4 weeks annual holidays with pay. At the same time, your outgoings like your mortgage and car repayments remain unchanged. Running a business can be a financial pressure cooker and business ownership is not for everyone.

There’s no definitive DNA profile for what makes a successful entrepreneur, however, there are some key characteristics that entrepreneurs share. Do you have the right personality, traits and skills to turn your idea into a viable business? As a guide, you need to be passionate about your products or services and ideally you should have industry knowledge and experience. Remember, you are taking a financial risk and it’s not for the faint hearted or novice. You need to be disciplined and decisive. If you’re a perfectionist think carefully about going down this path because you might let perfection get in the way of progress. Very few entrepreneurs get their business model right the first time so you need to be patient and listen to feedback from customers and even family members. At some point you might find you’ll need to pivot and adjust your offering to changes in the market or consumer behaviour. The pandemic forced many businesses to shift their focus to online sales with a click and collect option while others had to change to home delivery or provide take away only service.

There’s no definitive DNA profile for what makes a successful entrepreneur, however, there are some key characteristics that entrepreneurs share. Do you have the right personality, traits and skills to turn your idea into a viable business? As a guide, you need to be passionate about your products or services and ideally you should have industry knowledge and experience. Remember, you are taking a financial risk and it’s not for the faint hearted or novice. You need to be disciplined and decisive. If you’re a perfectionist think carefully about going down this path because you might let perfection get in the way of progress. Very few entrepreneurs get their business model right the first time so you need to be patient and listen to feedback from customers and even family members. At some point you might find you’ll need to pivot and adjust your offering to changes in the market or consumer behaviour. The pandemic forced many businesses to shift their focus to online sales with a click and collect option while others had to change to home delivery or provide take away only service.

You’ll need a degree of resilience because you’ll make mistakes and rejection is inevitable. Not every customer, client or patient is going to like your product or service. Not only that, not every customer is going to like you personally. While confidence is an asset for an entrepreneur, arrogance is a liability. Of course, having networking abilities and being resourceful will work in your favour.

Before you pull the trigger on your new business there are a number of important things to consider including:

1. Why?

It’s an important question because running a business is challenging and there are risks and financially, there are no guarantees. You’ll work harder and probably longer than any role you’ve had as an employee and with skin in the game you’ll experience stress because it’s your money on the line.

The potential for financial rewards can motivate entrepreneurs as can the enormous satisfaction and sense of achievement that can be derived from turning your idea into profitable business. You get to control your own destiny and enjoy the freedom plus you’ll probably aspire to earn more money than you would as an employee. Having said that, you need to be crystal clear about why you want to start your own business. It’s going to be hard and be prepared to weather the storm of long hours, slow early sales and limited cash flow. You’re going to have to upskill because all of a sudden you could be the receptionist, production manager, bookkeeper, marketing manager and debt collector in the business.

You could be a great technician but suddenly you’re the ‘front man’ of the business that requires sales skills. It’s probably going to be different to anything else you’ve done before so be prepared to learn and adapt. You’ll need to be agile and think on your feet.

2. Who?

Another important question is who will buy your goods and services? Who is your ideal type of customer and what are your niche markets? Where do they hangout and how do you tap into their communication channels? The more specific you can be about your customers and your niche markets, the easier it is to tailor your brand and marketing. Identifying your target market can also help you make decisions about your location, pricing, social media channels and your marketing.

3. Know Your Competitors

Research your competitors and understand why they have a share of the market. This could involve visiting their premises, ‘stalking’ them on social media or dissecting their website with a fine-tooth comb. Understand their point of difference. Identify their strengths and weaknesses which should help you identify gaps in the market and opportunities.

Research your competitors and understand why they have a share of the market. This could involve visiting their premises, ‘stalking’ them on social media or dissecting their website with a fine-tooth comb. Understand their point of difference. Identify their strengths and weaknesses which should help you identify gaps in the market and opportunities.

What systems and technology are they using? Who are they targeting and how are they marketing to them? Gather intelligence about their products, services, prices and marketing. With that knowledge, it’s time to nail your unique selling point and competitive advantage. What can you do better than your competitors? Figure out how your business offering is going to be different (and ideally better) to your competitors. Starting a business without a deep understanding of your competitors is a huge mistake. Know their pricing, marketing, strengths and weaknesses.

4. Know the Laws in Your Industry

Every industry has its own rules, regulations and idiosyncrasies. You need to understand the laws and comply with them. Do your research and prepare a checklist of essential licences, registrations and council permits. Don’t flout council or government rules because your business could come to a grinding halt. Remember, these regulations can vary from council to council and state to state so do your homework on things like employment law, occupational health and safety plus your commercial lease. Consult with us about taxation issues including business registrations, superannuation for staff and Single Touch Payroll.

5. Know Your Numbers

You need to quantify your financial expectations. If the numbers don’t stack up, the business may not be viable and you could be on the verge of burning yourself out and burning a lot of cash in the process. If the projected profits aren’t enough to justify the risk and hard work, it could be time to revise your pricing or offering or review your marketing. We can help you prepare a cash flow budget and profit & loss statement to help you prepare your projections for your first year of trading. We can also do some financial modelling to prepare some ‘what if’ calculations based on different price points.

You need to quantify your financial expectations. If the numbers don’t stack up, the business may not be viable and you could be on the verge of burning yourself out and burning a lot of cash in the process. If the projected profits aren’t enough to justify the risk and hard work, it could be time to revise your pricing or offering or review your marketing. We can help you prepare a cash flow budget and profit & loss statement to help you prepare your projections for your first year of trading. We can also do some financial modelling to prepare some ‘what if’ calculations based on different price points.

Using industry benchmarks, we can help you get an understanding of the performance of your competitors. For a start-up business these can be invaluable because you have no financial track record and there is a lot of estimates and guess work when preparing a budget.

When you’re in start-up mode it’s hectic. It’s easy to get caught up in product development or bury your head in researching your customer’s habits and your competitor’s performance. Too

often we see start-ups overestimate their revenue and underestimate their expenses. That often translates to a shortage of cash in the early stages which can be catastrophic. Your budget will also be a key document should you need to secure finance from a bank or third party.

6. The Price Is Right

Without doubt, one of the biggest mistakes that new business owners make is they try to get a toe hold in the market by undercutting their competitor’s prices. Being the cheapest is a risky strategy and while it might help attract some new customers, you run the risk of going broke.

Do your numbers and make sure you know your costs and break-even point. Again, we can help you do some financial modelling based on different price points that will help you understand the impact of different prices on your profitability.

Summary

The late Steve Jobs, Co-Founder, Chairman and CEO of Apple said, “Your work is going to fill a large part of your life, and the only way to be truly satisfied is to do what you believe is great work. And the only way to do great work is to love what you do.” He inspired a lot of entrepreneurs but following your passion doesn’t guarantee a lifetime of profits.

The late Steve Jobs, Co-Founder, Chairman and CEO of Apple said, “Your work is going to fill a large part of your life, and the only way to be truly satisfied is to do what you believe is great work. And the only way to do great work is to love what you do.” He inspired a lot of entrepreneurs but following your passion doesn’t guarantee a lifetime of profits.

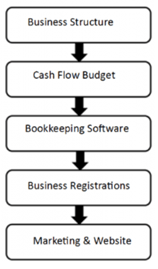

Starting a business is a process and there are numerous issues to consider including your choice of business structure and accounting software. You need to make decisions on your branding and marketing plus consider a range of business registrations. You’ll also need to think about your equipment requirements, finance and insurances. Of course, if you are looking to employ staff from the outset there are human resource issues including employment agreements, payroll software, workers compensation insurance plus superannuation guarantee obligations.

It can be a maze of issues that a business start-up needs to navigate through and as accountants we can clear the haze and provide advice on key issues including the preparation of a business plan, revenue forecasts, a cash flow budget, pricing, and insurances. We can also do some financial modelling to project your financial results based on different prices and costs.

Finally, if you’re looking to buy or sell a business, please don’t hesitate to contact us.

ATO Warns Business Owners About New JobKeeper Scam

The Australian Taxation Office (ATO) is warning business owners about the latest JobKeeper email scam to do the rounds, reminding SMEs to be wary of requests for their personal information.

This JobKeeper email scam involves a fake email that appears to come from the ATO, informing the recipients that the tax office is “checking all claims made through the Coronavirus JobKeeper Payments/Backing Business Incentive Scheme”.

The email asks business owners to reply to the email with “clear, high resolution” photos of the front and back of both their driver’s license and Medicare card.

“Don’t provide the information requested, and delete the email straight away,” the ATO advises. “If you receive a message from the ATO asking for your personal information, phone us on 1800 008 540 to make sure it’s legitimate. “You should never give out your personal information unless you’re sure of who you are dealing with.”

This is not the first time scammers have attempted to dupe business owners who are applying for or receiving JobKeeper payments. Back in May, the ATO warned businesses about a phone scam that involved individuals pretending to be from their organisation and asking for bank details so they could process the wage subsidy payments.

The ATO recommends reporting any emails that appear to be fraudulent to reportemailfraud@ato.gov.au.

2020-21 Federal Budget Summary

Treasurer Josh Frydenberg presented his second budget on October 6 in what was described as the, “most important budget since World War II”. As expected, there is massive expenditure to reboot and stimulate the economy after the economic devastation brought on by the coronavirus pandemic. The Budget outlined $85 billion of stimulus over four years, which is centered around immediate asset write-offs, income tax cuts and the extension of JobKeeper.

The Treasurer promised a budget that was “all about jobs”, and employment is indeed the theme of the suite of budget measures. For small and medium businesses, this translates to new wage subsidies for hiring young job-seekers and new apprentices, albeit with tight eligibility criteria. The Treasurer said, “There is no economic recovery without a jobs recovery,” and “There is no budget recovery without a jobs recovery.”

Frydenberg’s goal is to get businesses investing again, in new equipment and machinery, and new jobs. To this end, the government has announced a massive investment allowance that will enable nearly all Australian businesses to fully write-off all new assets purchased and used by June 2022.

We have summarised some of the key budget announcements including:

- the bringing forward of the individual tax relief planned for 2021, backdated to 1 July 2020

- a new loss carry-back for losses incurred up to June 2022 for companies with turnovers of up to $5 billion allowing most businesses to fully deduct any investment into depreciable assets until 30 June 2022, and

- a new JobMaker Hiring Credit for companies employing staff aged between 16 to 35 years old.

Personal Income Tax

As part of the Government’s JobMaker Plan, the tax cuts originally planned for July 2022 will be brought forward and backdated to July 1, 2020. They have lifted the threshold for the 19 per cent tax rate to $45,000 and the 32.5 per cent threshold to $120,000. The low and middle-income tax offset will also remain.

The Government’s Personal Income Tax Plan was designed to lower personal taxation and was to be implemented in three stages with Stage 1 implemented in June 2018. Stage 2 was to commence in 2021, however, this budget brings forward those tax cuts as well as a one-off additional benefit from the low and middle income tax offset in 2020/21. Stage 3 of the Government’s Personal Income Tax Plan remains in place for roll-out in 2024/25.

In 2020/21, low and middle income earners will receive tax relief of up to $2,745 for singles, and up to $5,490 for dual income families, compared with the 2017/18 rates. The majority of the tax benefit for 2020/21 will go to those on incomes below $90,000. Refer to the table below.

Tax Rate & Thresholds In 2017/18 Compared To 2020/21

Tax Rate & Thresholds In 2017/18 Compared To 2020/21

Superannuation

The Government has announced that, from July 1, 2021 they will implement a proposal to ‘staple’ an existing superannuation account to an individual as they move between jobs. The purpose of this measure is to reduce duplication of superannuation accounts for individuals when they change jobs and do not nominate their existing fund with their new employer (or otherwise do not consolidate their super if a new account is created for them).

This is a welcomed measure which reflects a proposal recently made by the Productivity Commission. We expect that the changes will improve the employee onboarding process for both employees and employers, and that future enhancements to payroll software will further simplify administrative processes on commencement of employment.

Business Taxation

IMMEDIATE DEDUCTIONS FOR BUSINESS ASSETS

Generally speaking, a business asset is ’depreciated’, meaning that a portion of the cost of the asset is deductible each year over the life of the asset. Under this measure, businesses with aggregated annual turnover of less than $5 billion will be able to deduct the full cost of eligible capital assets acquired from 7:30pm AEDT on 6 October2020 (Budget night) and first used or installed by June 30, 2022.

Generally speaking, a business asset is ’depreciated’, meaning that a portion of the cost of the asset is deductible each year over the life of the asset. Under this measure, businesses with aggregated annual turnover of less than $5 billion will be able to deduct the full cost of eligible capital assets acquired from 7:30pm AEDT on 6 October2020 (Budget night) and first used or installed by June 30, 2022.

Full expensing of the asset in the year of first use will apply to new depreciable assets and the cost of improvements to existing eligible assets. For small and medium sized businesses (with aggregated annual turnover of less than $50 million), full expensing will also apply to second-hand assets. The budget papers do not specify details of which assets will be ‘eligible’ assets for the purposes of this measure, but we expect that the definition will be broad.

The ‘immediate expensing’ applies to assets acquired after October 6, 2020. However, there is also an extension for businesses that acquired assets before budget night but had not yet used or installed them. Businesses that hold assets eligible for the enhanced $150,000 instant asset write-off will have an extra six months, until June 30, 2021, to first use or install those assets. Small businesses (with aggregated annual turnover of less than $10 million) can deduct the balance of their simplified depreciation pool at the end of the income year while full expensing applies. The provisions which prevent small businesses from re-entering the simplified depreciation regime for five years if they opt-out will continue to be suspended.

The benefits for your business:

- Immediate deductions for capital investments in assets to reduce the taxable income of the business in the year the asset is purchased

- Deductions allowed on an asset by asset basis

- Deductions for depreciation pool balances (i.e. immediate tax deduction for costs that would previously have been claimed over several years)

- If increased deductions for capital investments contribute to a company’s tax loss position, electing to apply the loss carry back provisions may allow the company to obtain a tax refund.

LOSS CARRY BACK

The Government will allow eligible companies to carry back tax losses from the 2020, 2021 or 2022 financial years to offset previously taxed profits in 2019 or earlier income years.

Corporate tax entities with an aggregated turnover of less than $5 billion can apply tax losses against taxed profits in a previous year, generating a refundable tax offset in the year in which the loss is made. The tax refund will be available on election by eligible businesses when they lodge their 2021 and 2022 income tax returns. Currently, companies are required to carry forward tax losses to offset them against profits in future years. Companies that do not elect to carry back losses under this measure can still carry forward losses as normal.

The tax refund will be limited by requiring that the amount carried back is not more than the earlier taxed profits and that the carry back does not generate a franking account deficit. In other words, the tax refund generated by the loss carry back provisions cannot exceed the company’s franking account balance.

This measure is designed to promote economic recovery by providing cash flow support to previously profitable companies that have fallen into a tax loss position as a result of the currently weaker economic conditions.

The loss carry-back provisions will also support the incentive for companies to invest under the investment incentive measures which will temporarily allow full expensing of capital acquisitions. If increased deductions for capital investments contribute to a company’s tax loss position, electing to apply the loss carry back provisions may allow the company to obtain a tax refund.

JOBMAKER HIRING CREDIT

The Government is introducing an incentive to encourage organisations to take on additional employees. This new incentive, the JobMaker Hiring Credit, will be available to eligible employers over 12 months from 7 October 2020 to 6 October 2021 for each additional new job they create for an eligible employee.

The Government is introducing an incentive to encourage organisations to take on additional employees. This new incentive, the JobMaker Hiring Credit, will be available to eligible employers over 12 months from 7 October 2020 to 6 October 2021 for each additional new job they create for an eligible employee.

Employer Eligibility – Eligible employers who can demonstrate that the new employee will increase overall employee headcount and payroll will receive:

- $200 per week if they hire an eligible employee aged 16 to 29 years or

- $100 per week if they hire an eligible employee aged 30 to 35 years.

The JobMaker Hiring Credit will be available for up to 12 months from the date of employment of the eligible employee with a maximum amount of $10,400 per additional new position created. Most employers would be eligible, however, employers must have an Australian Business Number (ABN), be up to date with their tax lodgement obligations, be registered for Pay As You Go (PAYG) withholding, report through Single Touch Payroll (STP) and cannot be claiming the JobKeeper Payment.

Employee Eligibility – To attract the JobMaker Hiring Credit, the employee must be in an additional job created from 7 October 2020. To demonstrate that the job is additional, specific criteria must be met. There must be an increase in:

- the business’ total employee headcount (minimum of one additional employee) from the reference date of 30 September 2020; and

- the payroll of the business for the reporting period, as compared to the three months to 30 September 2020.

The amount of the hiring credit claim cannot exceed the amount of the increase in payroll for the reporting period. To be eligible, the employee will need to have worked for a minimum of 20 hours per week, averaged over a quarter, and received the JobSeeker Payment, Youth Allowance (other) or Parenting Payment for at least one month out of the three months prior to when they are hired.

How to claim the Jobmaker Hiring Credit

The JobMaker Hiring Credit will be claimed quarterly in arrears by the employer from the Australian Taxation Office (ATO) from 1 February 2021. Employers will need to report quarterly that they meet the eligibility criteria.

INCREASING THE SMALL BUSINESS ENTITY TURNOVER THRESHOLD

The Government will expand access to a range of small business tax concessions by increasing the small business entity (SBE) turnover threshold for these concessions from $10 million to $50 million. Businesses with an aggregated annual turnover of $10 million or more but less than $50 million will for the first time have access to up to ten further small business tax concessions in three phases:

From 1 July 2020, eligible businesses will be able to immediately deduct certain start-up expenses and certain prepaid expenditure.

From 1 July 2020, eligible businesses will be able to immediately deduct certain start-up expenses and certain prepaid expenditure.- From 1 April 2021, eligible businesses will be exempt from the 47 per cent fringe benefits tax on car parking and multiple work-related portable electronic devices (such as phones or laptops) provided to employees.

- From 1 July 2021, eligible businesses will be able to access the simplified trading stock rules, remit pay as you go (PAYG) instalments based on GDP adjusted notional tax, and settle excise duty and excise-equivalent customs duty monthly on eligible goods under the small business entity concession.

Eligible businesses will also have a two-year amendment period apply to income tax assessments for income years starting from 1 July 2021, excluding entities that have significant international tax dealings or particularly complex affairs. The eligibility turnover thresholds for other small business tax concessions will remain at their current levels.

SINGLE NATIONAL BUSINESS REGISTRY

The federal government will allocate $420 million in this year’s budget to accelerate its plans to create a single national business registry, in a move designed to cut red tape for small business operators. The super registry will be operated by the Australian Taxation Office and will bring together the Australian Business Register and 31 other registers currently administered by the Australian Securities and Investments Commission.

IMPORTANT DISCLAIMER: This document contains general advice only and is prepared without taking into account your particular objectives, financial circumstances and needs. The information provided is not a substitute for legal, tax and financial product advice. Before making any decision based on this information, you should speak to a licensed financial advisor who should assess its relevance to your individual circumstances. While the firm believes the information is accurate, no warranty is given as to its accuracy and persons who rely on this information do so at their own risk. The information provided in this bulletin is not considered financial product advice for the purposes of the Corporations Act 2001.