- by Rebecca Gray

- April 22, 2020

- Uncategorized

Are You Losing Sleep Because of Your Business?

As a business owner you probably wear many hats. You could be filling part time roles as Receptionist, Bookkeeper, Webmaster, HR  Manager, Marketing Manager and even Cleaner. It can be a juggling act and it’s no surprise that most entrepreneurs are stressed and get less sleep than the rest of the general population.

Manager, Marketing Manager and even Cleaner. It can be a juggling act and it’s no surprise that most entrepreneurs are stressed and get less sleep than the rest of the general population.

Business owners are notorious for keeping files in their head and then they take them to bed which impacts on their sleep. In the digital and social era, a lot of business owners are in bed but wide awake between midnight and 3am thinking about cash flow, staffing issues and how to grow their business. According to the Brain and Mind Research Institute at the University of Sydney, about a third of the population report having trouble sleeping and about 10 per cent suffer from a sleep disorder.

Stress is one of the most common causes of insomnia and sleep deprivation is a form of torture that affects your mood and your productivity. It also makes you prone to sickness and clouds your ability to think clearly. As a business owner, you need to make decisions every day and a lack of sleep could be a recipe for disaster as your staff and customers are banking on you to make the right decisions. You also need a clear head to plan for the future and manage changes to your industry, new technology and emerging competition.

Of course, entrepreneurs are under constant financial pressure because your livelihood depends on the performance of your business. There’s always some uncertainty when running a business and ultimately, it’s your money and reputation on the line. Even a successful business doesn’t guarantee a good night’s sleep.

Generally speaking, self-employed people work longer hours than most of the population and they tend to make their business a priority over their personal health and wellbeing. Make no mistake, the strain on business owners is more than just financial. It can impact on your personal relationships as well as your physical and mental health.

TIME FOR A SWOT ANALYSIS?

If you’ve lost control of your business and you don’t know where you are heading, it’s time to stop and do some forward planning. A SWOT Analysis is designed to examine your Strengths, Weaknesses, Opportunities and Threats. Have a look at what’s working in the business, what’s not working and what aspects of your business need working on. After taking stock of your current position you can then formulate a plan to move forward.

FAILING TO PLAN IS PLANNING TO FAIL

You can reduce the uncertainty and chances of business failure by understanding your weaknesses and building on your strengths. The opportunities and threats to your business are usually external factors such as the economy, your competitors and changes in your industry. You need to understand your past performance and look at ways to improve your future performance. This means setting goals and then measuring your performance against those goals and key performance indicators (KPI’s).

We strongly believe in the saying, ‘Failing to Plan is Planning to Fail’. The planning process includes monitoring industry trends as well as changes in technology and consumer behaviour. Most industries are going through a digital transformation and the marketing landscape has changed. Google, websites and social media now dominate which has created uncertainty and new challenges for business owners. Marketing automation technology has altered the skill set required in the marketing department and if you’re still wearing the marketing manager’s hat, it could be time to seek assistance from a third party.

The real value in business planning is the reassurance it provides. You can be confident in the decisions you are making because your strategies align with your financial targets. You can track your progress against your financial projections and set timelines for implementation. This will make you accountable and most importantly, help you sleep at night.

If you need any help with your planning or are losing sleep worrying about your business, we invite you to contact us today.

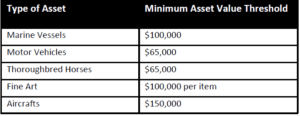

Have You Purchased a Luxury Car, Boat or Racehorse in the Last 5 Years?

Before you go out and purchase a luxury boat, car or thoroughbred horse – be aware the Tax Office is watching. In fact, their ‘lifestyle assets data-matching program’ involves gathering data from more than 30 insurance companies for these types of assets where the value is equal to or exceeds nominated thresholds.

The ATO have indicated that the classes of assets under review might be expanded as they identify and obtain data from other general and specialist insurers.

The ATO’s lifestyle assets data-matching program has actually been in place since February 2016 and under the program, they collect data on insurance policies for these types of asset. They have data from the 2015/16 year up to and including the 2019/20 year. The data includes the policy holder details (name, address, phone number, date of birth) plus the insurance policy details (policy number, start and end date, asset insured, physical location of the asset etc).

It is estimated that records of approximately 350,000 individuals will be obtained each financial year and the purpose of acquiring the data is to allow the ATO to identify potential tax evasion and fraud against the Commonwealth including:

- taxpayers accumulating (or improving) assets with insufficient income reported in their tax returns to show the financial means to pay for them

- income tax and capital gains tax (CGT) – taxpayers disposing of assets and not declaring the revenue and/or capital gains on those sales

- goods and services tax (GST) – taxpayers may be purchasing assets for personal use through their business or related entities and incorrectly claiming GST credits

- fringe benefits tax (FBT) – taxpayers may be purchasing assets through their business entities with no apparent connection with their business activities, but rather applying those assets to the personal enjoyment of an associate or employee giving rise to a fringe benefits tax liability

- self-managed super funds (SMSFs) may be acquiring assets but applying them to the benefit of the fund’s trustee or beneficiaries.

The ATO are required to comply with strict laws to protect your privacy when they collect data from other agencies and organisations for the purpose of their data matching programs. These laws include the Privacy Act 1988, the secrecy provisions of the Income Tax Assessment Act 1936 and the Taxation Administration Act 1953.

Why Lifestyle Assets?

The ATO claim that matching external data with tax return data ensures that people and businesses comply with their tax and super tax obligations. According to the Deputy Commissioner of Taxation, Deborah Jenkins, luxury and lifestyle items like private jets and yachts could indicate a discrepancy between someone’s real financial situation and what they might report in their income tax return. Ms Jenkins said, “If a taxpayer is reporting a taxable income of $70,000 to us but we know they own a three million dollar yacht, then this is likely to raise some red flags.”

The ATO claim that matching external data with tax return data ensures that people and businesses comply with their tax and super tax obligations. According to the Deputy Commissioner of Taxation, Deborah Jenkins, luxury and lifestyle items like private jets and yachts could indicate a discrepancy between someone’s real financial situation and what they might report in their income tax return. Ms Jenkins said, “If a taxpayer is reporting a taxable income of $70,000 to us but we know they own a three million dollar yacht, then this is likely to raise some red flags.”

“What we may discover is that some people have been declaring a level of income that simply does not add up when we compare it to the value of their assets like art, yachts, or aircraft.” She said the data could also help the ATO identify taxpayers who have made capital gains on the disposal of certain assets without declaring it, or those who bought the items for their own personal use only to declare it as a business asset and claim the GST credit. “With high value assets like fine art, there can be some significant capital gains made when these assets are sold, and capital gains tax may need to be paid on the sale or disposal of these items,” she said.

Of course, if you own and insure assets in these categories that are valued over the prescribed thresholds there’s no cause for alarm if your taxable income or other sources of funds support the purchase. If you suspect you’ve made an error in your return we recommend you contact us today.

What are the Tax Consequences of Different Business Structures?

The cornerstone of a business is your business structure. In Australia there are four main types of business structure – sole trader, trust, partnership or company. Each of these structures have different tax consequences that we will explore in this article.

Sole Trader

As a sole trader, you are effectively operating as an individual taxpayer and therefore your business profit is taxed at individual income tax rates. You report your business income in your individual tax return and the amount of tax you pay will depend on:

- Your level of business profit;

- Income from other sources including wages, interest; and

- any tax-deductible expenses you have incurred.

As a sole trader, you can offset any tax losses against your individual income. For example, if your business makes a loss you can offset that amount against your other income (salary etc.). Your taxable income is fundamentally your assessable income minus your tax deductions and the tax you pay in the 2019/20 financial year as an Australian resident is based on the table below. You’ll see there is no tax payable on the first $18,200 of income and every dollar over $180,000 is taxed at 45 cents (plus the Medicare levy).

As a sole trader, in certain situations you can receive a 50% discount on Capital Gains you need to include in your income. You must have owned the asset for 12 months or more and you can reduce the capital gain after applying all the capital losses for the tax year as well as other non-applied net capital losses from earlier years.

Company

Companies also lodge a company tax return, but they don’t get the benefit of a tax-free threshold. Companies pay a flat rate of tax on their taxable income and there are two different company income tax rates:

- the 27.5% base rate for companies that have an aggregated annual turnover of less than $50 million; and

- 30% rate that applies to companies that have an aggregated turnover of more than $50 million.

Unlike a sole trader, you can’t offset any tax losses against your individual income. Instead, the losses are carried forward to be offset against future profits. The flat rate of tax can be attractive to a highly profitable business – for example, if the taxable income was $500k the company would pay tax of $137,500 based on a 27.5% tax rate. A sole trader would pay tax of $198,097 on a $500k taxable income.

A company is a separate legal entity that can sue and be sued and as such, they can provide additional asset protection benefits. The shareholders own the shares in the company and the company can distribute their profits to shareholders by issuing dividends. These dividends are taxable in the hands of the shareholders; however, the Australian imputation system provides shareholders with a tax credit for the tax already paid by the company on those profits.

Companies do not receive the 50% Capital Gains Tax (CGT) discount like sole traders and individuals. However, if your company is a ‘small business entity’, you could be eligible for the small business CGT concessions if:

Companies do not receive the 50% Capital Gains Tax (CGT) discount like sole traders and individuals. However, if your company is a ‘small business entity’, you could be eligible for the small business CGT concessions if:

- the business has an aggregated turnover of less than $2M; or

- the company has a total net value of assets (including any affiliated entities like subsidiary companies) not exceeding $6M.

The small business CGT concessions allow you to disregard some or all of the capital gains made from the sale of an asset used in the course of carrying on a business, or an asset inherently connected with the business. If you sell an active asset that has been continuously owned for 15 years, and you are aged 55 or over and retiring, you can disregard the entire capital gain. If this 15-year exemption is not available, you can:

- reduce the capital gain by 50%;

- use the small business retirement exemption to reduce the capital gain for amounts up to $500,000; or

- defer all or part of the capital gain for two years or longer if you acquire a replacement active asset or spent money on making capital improvements on that active asset.

The purpose of these concessions is to boost your cashflow and potentially eliminate the tax payable on exiting a business.

Trust

A family trust (or discretionary trust) is an agreement where a person or a company agrees to hold assets for others’ benefit – usually their family members. It is often set up by families to own assets and they don’t pay tax. Trusts distribute their ‘net income’ and capital gains to their beneficiaries who in turn pay tax in their own right.

The word ‘discretionary’ relates to the trustee’s powers to distribute the net income and any capital gains made by the trust at their discretion each financial year. They decide how much income (if any) each beneficiary receives each year. By contrast, a unit trust distributes the trust income and capital gains based on the number of units held by the unit holders.

The word ‘discretionary’ relates to the trustee’s powers to distribute the net income and any capital gains made by the trust at their discretion each financial year. They decide how much income (if any) each beneficiary receives each year. By contrast, a unit trust distributes the trust income and capital gains based on the number of units held by the unit holders.

A family trust offers some level of protection over your personal assets. For example, in most situations, a creditor cannot access a trustee’s personal assets in the event of bankruptcy. Likewise, creditors cannot take assets held by a company trustee in the event of that company’s liquidation, subject to some exceptions.

It’s vitally important that you set up the trust with the right trustee and beneficiaries and annual tax planning is crucial to ensure the net income is distributed to the beneficiaries to minimise the tax liability.

Partnerships

Partnerships are formed when two or more people (up to 20 people) go into business together. Partnerships are governed by the Partnership Act 1958.

There are several forms of partnership including general partnerships and limited partnerships. A general partnership is where all the partners are equally responsible for the management of the business and each partner has unlimited liability for the debts of the business. A limited partnership is where the liability of one or more of the partners for the debts and obligations of the business is limited.

There are several forms of partnership including general partnerships and limited partnerships. A general partnership is where all the partners are equally responsible for the management of the business and each partner has unlimited liability for the debts of the business. A limited partnership is where the liability of one or more of the partners for the debts and obligations of the business is limited.

The partnership has its own tax file number and lodges an income tax return, however, it does not pay tax. The profit or losses of the partnership are divided among the partners and the partners pay tax in their own right. The partners entitlement to a share of the profit or loss will be based on the terms detailed in the Partnership Agreement. Subject to certain conditions, a partner’s share of any tax losses may be offset against other personal income.

A partnership is not a separate legal entity and partnerships allows tax incentives and tax-free capital gains concessions to be passed through the partners.

Personal Services Income

A word of warning regarding Personal Services Income (PSI) rules if you run your business by yourself. These rules apply where you produce your income mainly from your personal skills or efforts as an individual and the PSI rules apply in almost any industry or profession. Commonly, professionals in the financial industry, information technology consultants, engineers, construction workers and medical practitioners are caught under the PSI rules. If the ATO classifies your income as PSI, they will ignore your business structure and your business profits will be taxed as if you were an individual taxpayer. As a guide, if you have employees or you are selling goods, the PSI rules are unlikely to apply.

A word of warning regarding Personal Services Income (PSI) rules if you run your business by yourself. These rules apply where you produce your income mainly from your personal skills or efforts as an individual and the PSI rules apply in almost any industry or profession. Commonly, professionals in the financial industry, information technology consultants, engineers, construction workers and medical practitioners are caught under the PSI rules. If the ATO classifies your income as PSI, they will ignore your business structure and your business profits will be taxed as if you were an individual taxpayer. As a guide, if you have employees or you are selling goods, the PSI rules are unlikely to apply.

Summary

Your choice of business structure is a critical business decision and whenever we provide advice on business structures, we always take into account issues like:

- Minimisation of Income Tax

- Protection of Your Personal Assets

- The Potential Admission of New Business Partners or Investors

- Legal Requirements in your Industry

- Entitlement to Discount Capital Gains Tax Concessions

When evaluating alternative business structures, you also need to take into consideration the likely profitability of the business, the current tax position of all stakeholders and the risk profile of the industry. In some industries, participants often have a preference for the sole trader or company option. Consequently, we often find the business structure is a compromise based on the relative importance of these issues.

This article does not substitute for professional advice and every case is different. If you need advice on choosing the right structure for your business, we invite you to talk to us today.

Bushfire Support for Small Businesses

Prime Minister Scott Morrison announced a package of relief benefits for small businesses impacted by the recent bushfires.

Prime Minister Scott Morrison announced a package of relief benefits for small businesses impacted by the recent bushfires.

The package includes grant funding, concessional loans, tax relief and a dedicated contact point to help access the support. There are also financial counselling services that target small and family business owners to help them deal with the emotional and financial challenges ahead.

Grants: Top-up grants to eligible small businesses and non-profit organisations will be available under the Disaster Recovery Funding Arrangements. This program is uncapped and means that businesses and organisations that have sustained damage as a result of the fires can access up to $50,000 in grant funding (tax free).

Concessional Loans of up to $500,000 will be offered for businesses that have suffered significant asset loss or a significant loss of revenue. The loan would be for up to 10 years and used for the purposes of restoring or replacing damaged assets and for working capital. The loans will be available with a repayment holiday of up to two years, with no interest accruing during this period. The subsequent interest rate would be set at 50 per cent of the ten-year Commonwealth Government bond rate (currently around 0.6%).

Financial Support Line – The Government has pledged to establish the Small Business Bushfire Financial Support Line to provide information on the assistance and support available to small businesses in bushfire affected regions. You can contact them on 13 28 46 for assistance.

Tourism Recovery Package

The Government has pledged $76 million towards a tourism recovery package to protect jobs, small businesses and local economies affected by the bushfires. The Government’s initial tourism recovery package includes $20 million for a nationally coordinated domestic marketing initiative and $25 million for a global marketing campaign to drive international visitors.

The Government has pledged $76 million towards a tourism recovery package to protect jobs, small businesses and local economies affected by the bushfires. The Government’s initial tourism recovery package includes $20 million for a nationally coordinated domestic marketing initiative and $25 million for a global marketing campaign to drive international visitors.

- A further $10 million will be provided for a regional tourism events initiative across bushfire affected areas

- $9.5 million for an international media and travel trade hosting initiative

- $6.5 million to support tourism business’ attendance at the largest annual tourism trade event, the Australian Tourism Exchange, and

- $5 million for our diplomatic network to educate that our tourism, international education and export sectors are open for business.

Disaster Recovery Allowance

The Department of Human Services is providing support for people who have lost income as a direct result of the bushfires in New South Wales, Eastern Queensland, South Australia and Victoria through the Disaster Recovery Allowance.

The Department of Human Services is providing support for people who have lost income as a direct result of the bushfires in New South Wales, Eastern Queensland, South Australia and Victoria through the Disaster Recovery Allowance.

The Disaster Recovery Allowance is a short term payment to help you if a declared disaster directly affects your income. You can get it for a maximum of 13 weeks. It’s payable from the date you lose income as a direct result of the bushfires.

The maximum payment rate is the equivalent of Newstart or Youth Allowance, based on your circumstances. Your rate of payment will be affected by your income prior to and following the disaster.

Disaster Recovery Payment

The Department of Human Services is providing support for people adversely affected by the bushfires in New South Wales, Eastern Queensland, South Australia and Victoria through the Australian Government Disaster Recovery Payment.

The Australian Government Disaster Recovery Payment is a one-off payment to help you if a declared disaster significantly affects you. It’s not for minor damage or inconvenience.

You can choose to get this payment in 2 instalments if you prefer. If you’re eligible you will get $1,000 per adult and $400 for each child younger than 16.

Emergency Bushfire Support for Primary Producers

The Australian Government has committed $100 million in emergency grants for primary producers. Up to $75,000 is available to farmers, fishers and foresters. This is to cover costs for immediate and emergency needs not covered by existing insurance policies.

The Australian Government has committed $100 million in emergency grants for primary producers. Up to $75,000 is available to farmers, fishers and foresters. This is to cover costs for immediate and emergency needs not covered by existing insurance policies.

State Government Bushfire Tax Relief Measures

The Victorian, South Australian and New South Wales governments have announced a range of tax relief measures for individuals and businesses directly affected by bushfires. The measures commence immediately.

These measures include:

- Stamp Duty relief for the purchase of replacement homes and motor vehicles,

- Land Tax relief for land in affected areas, and

- Payroll Tax relief for employers located in affected areas or whose employees are involved in bushfire-fighting efforts.

If you have been affected by the bushfires, please contact us for assistance in determining what relief from State taxes may be available.

If you have been affected by the bushfires, please contact us for assistance in determining what relief from State taxes may be available.

Thinking of Selling Your Business?

Selling your business can be a lengthy and complex process. There are a number of steps in the sale process including negotiating the price and terms, drafting the contract, due diligence, contract review, financial settlement and handover.

The sale can include a variety of different assets such as goodwill, intellectual property (e.g. trademarks), real property interests (like a commercial lease), stock, furniture and fittings, contracts with suppliers and licences. Once you’ve agreed on the sale terms you still need to formalise the sale with a legal contract and at that point, a lot of issues can emerge that can stall or halt proceedings. With the contract, sometimes it’s the devil in the detail that can derail the sale. The contract should cover every possible scenario including issues that weren’t addressed at the negotiation stage.

A lot of entrepreneurs make rookie mistakes when selling their business that potentially cost them thousands, if not tens of thousands of dollars. Below are four common errors to avoid.

Error 1: Failing to Plan

Here’s some advice that also serves as a warning for business owners – all the years spent building and growing your business can amount to very little if you don’t plan your exit. Timing is everything and you never know when the perfect buyer might knock on your door. Holding out too long or holding on for the right price could mean you lose that ideal buyer.

You need to be investor ready that means making sure your bookkeeping and financials are up to date. The most valuable asset in some businesses is their customer database and CRM system so make sure they are current. Investor ready also means adopting the latest technology so don’t defer the implementation of new systems or leave the buyer to install the new technology. If you procrastinate it could impact on your sale price. Buyers want to invest in a business that is set up for success.

In planning the sale, you need to be crystal clear about why you are selling the business because prospective buyers will question your sale motive. If the business is flat lining or in decline, they will assume you are selling a distressed or failing business that gives them the edge in price negotiations.

Error 2: Price Expectations

As we all know, price is important! An unrealistic price tag can stall or kill the sale. If the business is treading water and producing no profit, then you might be overestimating the value. The price, in many industries, is based on a multiple of the profit or revenue so again you need to have accurate financial statements to ascertain the true market value.

As we all know, price is important! An unrealistic price tag can stall or kill the sale. If the business is treading water and producing no profit, then you might be overestimating the value. The price, in many industries, is based on a multiple of the profit or revenue so again you need to have accurate financial statements to ascertain the true market value.

Price can also be impacted by the trend in revenue and profits. As mentioned below, don’t wind down and take your foot off the pedal because buyers want a business that is growing not slowing. If you’ve lost motivation, then start the sale planning process immediately. When pricing the business consult with brokers and your industry bodies. Research industry benchmarks and examine other business sales in your industry.

Error 3: Keep Your Foot on the Pedal

Another big mistake vendors make when they decide to sell is taking their foot off the pedal. They relax, scale back their marketing spend, and the business slows. As you know, it can take months or even years to sell a business and buyers will gravitate away from a business in decline or they will look to negotiate the price down.

Error 4: The Wrong Buyer

The truth is a lot of business sales turn sour. Shortly after takeover, the buyer might elect to rebrand, increase the prices or change suppliers which could have a catastrophic effect on the business. When buying a business many people recommend that you ‘don’t rock the boat’ and make too many changes because so much can go wrong. The new owners might lack business and industry experience or could make poor management decisions like removing key staff or appointing unsuitable new staff.

The sale terms are obviously critical, and you might get only a small percentage of the sale price upfront. The balance of the funds might be withheld over several years subject to turnover and if the business crashes under the new management team, you could be left out of pocket. While it’s always tempting to accept the first offer for the business, make sure you do some due diligence on the buyer. Will they ‘rock the boat’ and make wholesale changes? Will they connect with your customers? Do they have the industry experience?

The sale terms are obviously critical, and you might get only a small percentage of the sale price upfront. The balance of the funds might be withheld over several years subject to turnover and if the business crashes under the new management team, you could be left out of pocket. While it’s always tempting to accept the first offer for the business, make sure you do some due diligence on the buyer. Will they ‘rock the boat’ and make wholesale changes? Will they connect with your customers? Do they have the industry experience?

When making the sale decision, is the offer in line with your valuation? The first offer may not be the best offer, but it could be some time before another buyer makes an offer. The economy could dip, and the bottom could fall out of the market, so think carefully and talk to your advisory team. The right accountant, solicitor and business broker can make a big difference.

If you’re contemplating selling your business or looking to plan the sale, we invite you to contact us today. We can help you navigate your way through the process and of course explain the tax implications of the sale including any exposure to capital gains tax.

IMPORTANT DISCLAIMER: This document contains general advice only and is prepared without taking into account your particular objectives, financial circumstances and needs. The information provided is not a substitute for legal, tax and financial product advice. Before making any decision based on this information, you should speak to a licensed financial advisor who should assess its relevance to your individual circumstances. While the firm believes the information is accurate, no warranty is given as to its accuracy and persons who rely on this information do so at their own risk. The information provided in this bulletin is not considered financial product advice for the purposes of the Corporations Act 2001.