- by Rebecca Gray

- May 24, 2024

- Superannuation tax management Bookkeeping business startup

2024-25 Federal Budget

2024–25 Federal Budget Highlights

The Federal Treasurer, Dr Jim Chalmers, handed down the 2024–25 Federal Budget at 7:30 pm (AEST) on 14 May 2024.

Described as a “responsible Budget that helps people under pressure today”, the Treasurer has forecast a second consecutive surplus of $9.3 billion. The main priorities of the government, as reflected in the Budget, are helping with the cost of living, building more housing, investing in skills and education, strengthening Medicare and responsible economic management to help fight inflation.

The key tax measures announced in the Budget include extending the $20,000 instant asset write- off for eligible businesses by 12 months until 30 June 2025, introducing tax incentives for hydrogen production and critical minerals production, strengthening foreign resident CGT rules and penalising multinationals that seek to avoid paying Australian royalty withholding tax.

The Budget also includes various amendments to previously announced measures, as well as a number of income tax measures that have already been enacted prior to the Budget announcement, including:

- the revised stage 3 personal income tax cuts (enacted by the Treasury Laws Amendment (Cost of Living Tax Cuts) Act 2024 (Act No 3 of 2024))

- Medicare levy and surcharge threshold changes (enacted by the Treasury Laws Amendment (Cost of Living—Medicare Levy) Act 2024 (Act No 4 of 2024)), and

- a specific exemption for Australian plantation forestry entities from the new earnings- based rules introduced as part of thin capitalisation reforms (enacted by the Treasury Laws Amendment (Making Multinationals Pay Their Fair Share—Integrity and Transparency) Act 2024 (Act No 23 of 2024)).

These enacted measures have not been discussed in detail in this report.

The government anticipates that the tax measures put forward will collectively improve the Budget position by $3.1 billion over a 5-year period to 2027–28.

The full Budget papers are available at www.budget.gov.au and the Treasury ministers’ media releases are available at ministers.treasury.gov.au.

The tax, superannuation and social security highlights are set out below.

Income tax

- The instant asset write-off threshold of $20,000 for small businesses applying the simplified depreciation rules will be extended for 12 months until 30 June 2025.

- The foreign resident CGT regime will be strengthened for CGT events commencing on or after 1 July 2025.

- A critical minerals production tax incentive will be available from 2027–28 to 2040–41 to support downstream refining and processing of critical minerals.

- A hydrogen production tax incentive will be available from 2027–28 to 2040–41 to producers of renewable hydrogen.

- The minimum length requirements for content and the above-the-line cap of 20% for total qualifying production expenditure for the producer tax offset will be removed.

- A new penalty will be introduced from 1 July 2026 for taxpayers who are part of a group with more than $1 billion in annual global turnover that are found to have mischaracterised or undervalued royalty payments.

The Labor government’s 2022–23 Budget measure to deny deductions for payments relating to intangibles held in low- or no-tax jurisdictions is being discontinued.

The Labor government’s 2022–23 Budget measure to deny deductions for payments relating to intangibles held in low- or no-tax jurisdictions is being discontinued.- The start date of a 2023–24 Budget measure to expand the scope of the Pt IVA general anti- avoidance rule will be deferred to income years commencing on or after assent of enabling legislation.

- Income tax exemptions for World Rugby and/or related entities for income derived in relation to the Rugby World Cup 2027 (men’s) and Rugby World Cup 2029 (women’s).

- Deductible gift recipients list to be updated.

Social security

- Social security deeming rates will be frozen at their current levels for a further 12 months until 30 June 2025.

- Carer payment recipients will have greater flexibility with their participation requirements.

- Eligibility for the higher rate of Jobseeker payment will be extended to single recipients with a partial capacity to work of zero to 14 hours per week.

- The maximum rates of the Commonwealth Rent Assistance will increase by 10% from 20 September 2024.

- Funding will be provided to implement a social security means test treatment for military invalidity payments affected by the Full Federal Court’s decision of FC of T v Douglas 2020 ATC 20

-773; [2020] FCAFC 220. - Funding will be provided to enable Australia to enter into a bilateral social security agreement with Uruguay.

- Foreign investors will be allowed to purchase established build-to-rent properties with a lower foreign investment fee.

Superannuation

Superannuation will be paid on government-funded paid parental leave (PPL) for parents of babies born or adopted on or after 1 July

Superannuation will be paid on government-funded paid parental leave (PPL) for parents of babies born or adopted on or after 1 July

2025.- The Fair Entitlements Guarantee Recovery Program will be recalibrated to pursue unpaid superannuation entitlements owed by employers in liquidation or bankruptcy from 1 July 2024.

Tax administration

- The ATO will be given a statutory discretion to not use a taxpayer’s refund to offset old tax debts on hold.

- Indexation of the Higher Education Loan Program (and other student loans) debt will be limited to the lower of either the Consumer Price Index or the Wage Price Index, effective from 1 June 2023.

- A pilot program of matching income and employment data of migrant workers will be conducted between the Department of Home Affairs and the ATO.

A new ATO compliance taskforce will be established to recover tax revenue lost to fraud while existing compliance programs will be extended.

A new ATO compliance taskforce will be established to recover tax revenue lost to fraud while existing compliance programs will be extended.- The ATO will have additional time to notify a taxpayer if it intends to retain a business activity statement refund for further investigation.

- The 2019–20 Budget measure “Black Economy — Strengthening the Australian Business Number system” will not proceed.

GST

- Refunds of indirect tax (including GST, fuel and alcohol taxes) will be extended under the Indirect Tax Concession Scheme.

Excise and customs duty

- Tariffs identified as a nuisance across a range of imported goods will be removed from 1 July 2024.

- The start dates for certain components of a measure to streamline excise administration for fuel and alcohol announced in the Coalition government’s 2022–23 Budget will be deferred.

2024 Year End Tax Planning Guide

Areas of tax planning to be considered:

- Key Tax Minimisation Strategies.

- Round Up of Other Year End Tax Issues.

- Other Tax Effective Strategies for Businesses to Consider.

- Superannuation Tax Planning Opportunities.

- Immediate Write Off & Temporary Full Expensing for Individual Small Business Assets.

Key Tax Minimisation Strategies

1. Delay Deriving Assessable Income

1. Delay Deriving Assessable Income

One effective strategy is to delay deriving your income until after June 30, 2024. Consider the following:

a. Delaying the Timing of the Derivation of Income until after June 30.

b. Timing of Raising Invoices for Incomplete Work (Businesses)

This tactic needs thought as it can adversely affect your cash flow and lead to issues better left alone. Invoices raised before 1-7-2024 are income in this financial year. Please note, not banking amounts received before June 30 until after June 30 do NOT qualify because the income is deemed to have been earned when the money is received, or the goods or services are provided (depending on whether you are on a cash or accruals basis of accounting).

- •Cash Basis Income – Some income is taxable on a cash receipts basis rather than on an accruals basis (e.g. rental income or interest income in certain cases). You should consider whether some income can be deferred.

- Consider delaying your invoices to customers until after July 1 which will push the generation of the income into the next financial year and defer the tax payable on it. If you operate on a cash basis, you simply need to delay receiving the money from your customers until after June 30.

- Lump Sum Amounts – Where a lump sum is likely to be received close to the end of a financial year, you should consider whether this amount (or part thereof) can be delayed or spread over future periods.

2. Bringing Forward Deductible Expenses or Losses

Prepayment of Expenses In some circumstances, small businesses and individuals who derive passive type income (such as rental income and dividends) should consider pre-paying expenses prior to 30 June 2024. A tax deduction can be brought forward into this financial year for expenses like:

- Employee Superannuation Payments including the 11% Superannuation Guarantee Contributions for the June 2024

quarter (any such contribution MUST be received by the Superannuation Fund by June 30, 2024 if a tax deduction is to be claimed). - Superannuation for Business Owners, Directors, and Associated Persons.

- Wages, bonuses, commissions, and allowances.

- Contractor Payments.

- Travel and accommodation expenses.

- Trade creditors.

- Rent for July 2024 (and possibly future additional months – speak to your accountant to see if this is possible in your case).

- Insurances including Income Protection Insurance.

- Printing, Stationery and Office Supplies.

- All forms of advertising and promotion.

- Utility Expenses – Telephone, Electricity & Power.

- Motor Vehicle Expenses – Registration and Insurance.

- Accounting Fees.

- Subscriptions and Memberships to Professional Associations and Trade Journals.

- Repairs and Maintenance to Investment Properties.

- Self Education Costs.

- Home Office Expenses – desk, chair, computers etc. This area of expenses has changed significantly in recent years. Speak to your accountant about your situation.

- Donations to deductible gift recipient organisations.

- If appropriate, consider prepaying any deductible investment loan interest. This could include interest payments on an investment loan for either an investment or commercial property or an investment portfolio you hold.

A deduction for prepaid expenses will generally be allowed where the payment is made before 30 June 2024 for services to be rendered within a 12-month period. While this strategy can be effective for businesses operating on a cash basis (not accruals basis).

A deduction for prepaid expenses will generally be allowed where the payment is made before 30 June 2024 for services to be rendered within a 12-month period. While this strategy can be effective for businesses operating on a cash basis (not accruals basis).

3. Superannuation Contributions

Some low or middle-income earners who make personal (after-tax) contributions to a superannuation fund may be entitled to the government co-contribution. The amount of government co-contribution will depend on your income and how much you contribute.

4. Capital Gains/Losses

Note that the contract date (not the settlement date) is usually the key sale date for capital gains tax purposes. Here are several important points regarding the management of capital gains and capital losses on a sale of your assets from a tax planning perspective:

i. If possible, consider deferring the sale of an asset with an expected capital gain (and applicable capital gains tax liability) until it has been held for 12 months or longer. By doing so, you could reduce your personal income tax. For example, if you hold an asset for under 12 months, any capital gain you make may be assessed in its entirety upon the sale of that asset.

i. If possible, consider deferring the sale of an asset with an expected capital gain (and applicable capital gains tax liability) until it has been held for 12 months or longer. By doing so, you could reduce your personal income tax. For example, if you hold an asset for under 12 months, any capital gain you make may be assessed in its entirety upon the sale of that asset.

ii. A capital gain will be assessable in the financial year that it’s realised.

iii. If possible, consider deferring the sale of an asset with an expected capital gain (and applicable capital gains tax liability) to a future financial year. By doing so, you could help reduce your personal income tax for the current financial year. This could also be of benefit if, for example, you expect that your income will be lower in future financial years compared to the current financial year.

iv. If appropriate, consider offsetting a realised capital gain with an existing capital loss (carried forward or otherwise) or bringing forward the sale of an asset currently sitting at a loss. By doing so, you could reduce your personal income tax in this financial year. Note that a capital loss can only be used to offset a capital gain.

iv. If appropriate, consider offsetting a realised capital gain with an existing capital loss (carried forward or otherwise) or bringing forward the sale of an asset currently sitting at a loss. By doing so, you could reduce your personal income tax in this financial year. Note that a capital loss can only be used to offset a capital gain.

Accounts Payable (Creditors) – If you operate on an accruals basis and services have been provided to your business, ensure that you have an invoice dated June 30, 2024, or before so you can take up the expense in you accounts for the year ended 30th June 2024.

Immediate Write-Off For Individual Small Business Assets & Temporary Full Expensing

IMPORTANT and confirmed by the ATO on 22-5-24. There is some confusion about this deduction due to legislation being held up in The House of Representatives. The aim is to increase the current limit of $1,000 to $20,000. However, an amendment seeking to increase this deduction to $30,000 has been the cause for delay. There are only seven more sitting days (28th May to 6th June) before time is almost too limited for small businesses to invest. ‘As it stands today, businesses with a turnover of less than $10 million can claim the instant asset write-off for assets valued less than $1,000 and that are first used or installed between July 1, 2023, and June 30, 2024.’

Conditions for accessing the instant asset write-off threshold for small business entities in the 2024 income year include:

Conditions for accessing the instant asset write-off threshold for small business entities in the 2024 income year include:

- It only relates to Plant, Equipment and Vehicles. It does NOT relate to Capital improvements to buildings.

- The items can be new or second hand. You can have paid cash, or they can be financed.

- The entity must operate a business during the 2024 income year.

- Its aggregated annual turnover must be under $10 million, based on either the current or previous year’s figures.

- Choosing to apply the simplified depreciation rules for the 2024 income year is necessary.

- The asset’s cost must be less than $1,000. $20,000 if legislation is passed.

- The asset must be first used, or installed and ready for use, for a taxable purpose between July 1, 2023, and June 30, 2024.

It’s crucial to understand that if a small business entity opts out of applying the simplified depreciation rules for the 2024 income year, they won’t have access to the instant asset write-off rules, regardless of meeting other basic conditions. The instant asset write-off threshold applies per asset, allowing small business entities to potentially deduct the full cost of multiple assets throughout the 2024 year, provided each asset’s cost is less than $1,000. Additionally, the $1,000 threshold applies to determining whether the full pool balance is written off in the 2024 income year.

Eligible assets for the instant asset write-off rules are those falling within the depreciation provisions. Capital improvements to buildings under the capital works rules are excluded. Assets costing $1,000 or more, which cannot be immediately deducted, can still be included in the small business general pool, and depreciated at 15% in the first income year and 30% in subsequent income years.

We have a checklist to help you get your documents together in preparation for the end of the financial year. Contact us today to get your copy.

Checklist of Other Year End Tax Issues

In addition to the tax planning opportunities, there are a number of obligations in relation to the end of the financial year which should be considered:

If you use a Motor Vehicle in producing your income you may need to:

- Record Motor Vehicle Odometer readings at 30 June 2024

- Prepare a log book for 12 continuous weeks if your existing one is more than 5 years old. Please note, if you commence the logbook prior to June 30, 2024, the usage determined will still be appropriate for the whole of 2023/24. As such, it is not too late to start preparing one for the current financial year. (Tip – the ATO has an App that can assist with keeping records such as business use logbooks – https://www.ato.gov.au/General/Online-services/ATO-app/myDeductions/?=Redirected_URL

If you have started an account-based pension:

If you have started an account-based pension:

Ensure that you have withdrawn the annual minimum required.

If you are in business or earn your income through a Company or Trust:

- Employer Compulsory Superannuation Obligations: The deadline for employers to pay Superannuation Guarantee Contributions for the 2023/24 financial year is the 28 July 2024. However, if you want to claim a tax deduction in the 2023/24 tax year the super fund (or Small Business Superannuation Clearing House) must receive the contributions by 30 June 2024. You should therefore avoid making contributions at the last minute because processing delays could deny you a significant tax deduction in this financial year.

- For Private Company – Div 7A Loans – Business owners who have borrowed funds from their company in prior years must ensure that the appropriate principal and interest loan repayments are made by 30 June 2024. Current year loans must be either paid back in full or have a loan agreement entered into before the due date of lodgement of the company return. Failure to comply risks having it counted as an unfranked dividend in the individual’s tax return

- Trustee Resolutions – ensure that the Trustee Resolutions on how the income from the trust is distributed to the beneficiaries are prepared and signed before June 30, 2024 for all Discretionary (“Family”) Trusts. If a valid resolution hasn’t been executed by this date, the default beneficiaries become entitled to the trust’s income and are then subject to tax. Income derived but not distributed by the trust will mean the trust will be assessed at the highest marginal rate on this income.

- Preparation of Stock Count Working Papers at June 30, 2024.

- Preparation and reconciliation of Employee PAYG Payment Summaries (formerly known as Group Certificates). Note you are not required to supply your employees with payment summaries for amounts you have reported and finalised through Single Touch Payroll.

From 1 July 2024:

The compulsory Super Guarantee Contribution rate increases from 11 % to 11.5% from July 1, 2024.

The compulsory Super Guarantee Contribution rate increases from 11 % to 11.5% from July 1, 2024.

Company Tax Rates For Small Businesses

The company tax rate for base rate entities with less than $50 million turnover was 25% for the 2024 financial year where it as:

- An aggregated turnover less than the aggregated turnover threshold ($50 million)

- 80% or less of their assessable income is base rate entity passive income – this replaces the requirement to be carrying on a business.

Other Tax Effective Strategies For Businesses

BUSINESSES SHOULD ALSO CONSIDER THE FOLLOWING ITEMS

- Stock Valuation Options – Review your Stock on Hand and Work in Progress listings before June 30 to ensure that it is valued at the lower of Cost or Net Realisable Value. Any stock that is carried at a value higher than you could realise on sale (after all costs associated with the sale) should be written down to that Net Realisable Value in your stock records.

- Write-Off Bad Debts – if you operate on an accruals basis of accounting (as distinct from a cash basis) you should write off bad debts from your debtors listing before June 30. A bad debt is an amount that is owed to you that you consider is uncollectable or not economically feasible to pursue collection. Unless these debts are physically recorded as a ‘bad debt’ in your system before 30th June 2024, a deduction will not be allowable in the current financial year.

- Repairs and Maintenance Costs – Where possible, and cash flow allows, consider bringing these repairs forward to before June 30. If you don’t understand the distinction between a repair and a capital improvement please consult with us because some capital improvements may not be tax deductible in the current year and could be claimable over a number of years as depreciation.

- Obsolete Plant and Equipment – should be scrapped or decommissioned prior to June 30, 2024 to enable the book value to be claimed as a tax deduction.

Superannuation Tax Planning Opportunities

Superannuation Tax Planning Opportunities

CONCESSIONAL CONTRIBUTION CAP OF $27,500 FOR EVERYONE

The tax-deductible superannuation contribution limit or cap is $27,500 for all individuals regardless of their age for the 2023/24 financial year. This will be increased to $30,000 from the 1st July 2024. If eligible and appropriate, consider making the most of your 2023/24 financial year annual concessional contributions cap with a concessional contribution. Note that other contributions such as employer Superannuation Guarantee Contributions (SGC) and salary sacrifice contributions will have already used up part of your concessional contributions cap.

CARRY FORWARD CONCESSIONAL CONTRIBUTIONS

If your total superannuation balance as at June 30, 2023 was less than $500,000 you may be in a position to carry-forward unused concessional caps for up to 5 years. Members can access their unused concessional contributions caps on a rolling basis for five years and amounts carried forward that have not been used after five years will expire. The advantage of making the maximum tax-deductible superannuation contribution before June 30, 2024 is that superannuation contributions are taxed at between 15% and 30%, compared to personal tax rates of between 32.5% and 45% (plus 2% Medicare levy) for an individual taxpayer earning over $45,000.

Typically, self-employed individuals and those who earn their income primarily from passive sources like investments make their super contributions close to the end of the financial year to claim a tax deduction. However, individuals who are employees may also use this strategy and those who might want to take advantage of this opportunity.

NON -CONCESSIONAL SUPER CONTRIBUTIONS

If eligible and appropriate, consider utilising all or part of your 2023/24 financial year annual non-concessional contributions cap by making a non-concessional contribution for up to $110,000 for the 2024 financial year. This will be increased to $120,000 from 1 July 2024.

If eligible and appropriate, consider utilising all or part of your 2023/24 financial year annual non-concessional contributions cap by making a non-concessional contribution for up to $110,000 for the 2024 financial year. This will be increased to $120,000 from 1 July 2024.

If you are not currently in a non-concessional contributions bring forward period, consider whether you may be in a position to ‘bring-forward’ your non-concessional contributions caps for the 2024/25 and 2025/26 financial years.

GOVERNMENT CO-CONTRIBUTION TO YOUR SUPERANNUATION

The Government co-contribution is designed to boost the superannuation savings of low and middle-income earners who earn at least 10% of their income from employment or running a business. If your income is within the thresholds listed in the table below and you make a ‘non-concessional contribution’ to your superannuation, you may be eligible for a Government co-contribution of up to $500.

To be eligible you must be under 71 years of age as at June 30, 2024. In 2023/24, the maximum co-contribution is available if you contribute $1,000 and earn $43,445 or less. A lower amount may be received if you contribute less than $1,000 and/or earn between $42,016 and $57,016.

The matching rate is 50% of your contribution and additional eligibility include: having a total superannuation balance of less than $1.9 million on 30 June of the year before the year the contributions are being made having not exceeded your non-concessional contributions cap in the relevant financial year.

TRANSITION TO RETIREMENT

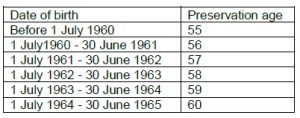

If you don’t want to fully retire and would like to reduce your working hours you can take advantage of what is known as “Transition to Retirement” TTR. This means that providing you have reached your preservation age you can elect to keep working full time or part- time and take money out of your super to supplement your income. This is popular for those who want to scale down their working hours rather than retiring.

If you don’t want to fully retire and would like to reduce your working hours you can take advantage of what is known as “Transition to Retirement” TTR. This means that providing you have reached your preservation age you can elect to keep working full time or part- time and take money out of your super to supplement your income. This is popular for those who want to scale down their working hours rather than retiring.

When you are receiving a TRT pension you can still work and claim a tax deduction for concessional contributions into super currently $27,500 for the 2024 financial year, and then increasing to $30,000 from the 1st July 2024.

If you decide to implement a TTR strategy, you must withdraw a minimum amount currently 4% for someone aged 60 (based on age) from your superannuation account balance up to a maximum of 10%.

If you are under 60 any amount you withdraw will be subject to tax at your marginal rate of tax. You will also be entitled to receive a tax rebate of 15%. After the age of 60, the good news is that any amount you withdraw is TAX FREE!

Case Study 1 : Bill reduces his work hours

Bill just turned 60 and earns $50,000 a year before tax. He decides to ease into retirement by reducing his work to three days a week. This means his income will decrease to $30,000. Bill transfers $155,000, of his super to a transition to retirement pension and withdraws $9,000 each year, tax-free. This replaces some of his lost pay.

Case Study 2: Sue reduces her tax

Sue is 60 and earns $100,000 a year. She intends to keep working full-time for at least another five years. Sue transfers $200,000 from her super to an account-based pension so she can start a TTR strategy.

Sue is 60 and earns $100,000 a year. She intends to keep working full-time for at least another five years. Sue transfers $200,000 from her super to an account-based pension so she can start a TTR strategy.

She salary sacrifices into her super. This will reduce her income tax, but also her take-home pay. She tops up her income by withdrawing up to 10% of her TTR pension balance each year.

As you can see the TRT strategy is very useful for people wanting to work less and supplement their income by drawing from superannuation.

ACCOUNT BASED PENSIONS

If you are aged 60 + and retired or 65+ and still working, There are significant tax advantages in taking an Account Based Pension from your super. Not only are the withdrawals you make tax-free, but also the earnings within your superannuation fund are tax-free to 1.9 million dollars.

Although you must withdraw, the minimum amount must be paid each year for pensions as per the table below, there are no limits on the amount you can withdraw.

The minimum amount for ages:

- Under 65 is 4%

- 65 to 74 is 5%

- 75 to 79 is 6%

- 80 to 84 is 7%

To put in place an account-based pension, you will need to speak to your superannuation fund provider.

SELF-MANAGED SUPERANNUATION

A Self-Managed Superannuation Fund (SMSF) can provide significant tax savings, but they don’t suit everyone. There are significant regulations surrounding the management and administration of SMSF’s. With the end of the financial year approaching, now is a good time to discuss the pros and cons of establishing your own SMSF. It might be appropriate to establish an SMSF in conjunction with other tax planning opportunities.

IMPORTANT DISCLAIMER: This document contains general advice only and is prepared without taking into account your particular objectives, financial circumstances and needs. The information provided is not a substitute for legal, tax and financial product advice. Before making any decision based on this information, you should speak to a licensed financial advisor who should assess its relevance to your individual circumstances. While the firm believes the information is accurate, no warranty is given as to its accuracy and persons who rely on this information do so at their own risk. The information provided in this bulletin is not considered financial product advice for the purposes of the Corporations Act 2001.