- by Rebecca Gray

- October 26, 2023

- management Bookkeeping business startup Superannuation tax

Contractor Payments (TPAR) are Increasing on the ATO’s Radar

The ATO has drawn a line in the sand for reporting contractor payments and warns tardy businesses that missing its deadline will involve penalties and set off alarm bells about dodgy behaviour.

The ATO has drawn a line in the sand for reporting contractor payments and warns tardy businesses that missing its deadline will involve penalties and set off alarm bells about dodgy behaviour.

It is estimated that the shadow economy costs Australia $12.4 billion a year in lost taxes. It is the job of the ATO to recover this money and reports such as the Taxable Payments Annual Report (TPAR), due by 28th August, and other ATO systems are increasingly effective at clawing this money back.

It is getting harder for businesses to hide from the ATO, like using cash payments to avoid tax, as the TPAR data gives the ATO the extra puzzle pieces it needs to catch-out such dishonest behaviour.

All lost taxes have to be made up by those business and individuals who do not indulge in activities such as paying cash, payments that temp some to pay less tax than they should. It may seem like a win to some, but it is a penalty for every honest business and individual.

The ATO says, “If you are asking for cash and not declaring it to the ATO, you will receive a ‘please explain’ and you will be penalised. It’s not a matter of ‘if’, it’s a matter of ‘when’.”

The TPAR system recorded $400 billion in payments made to almost 1.1 million contractors in 2022–23.

The typical businesses paying contractors included those in building and construction, cleaning, courier and road freight, information technology and security, and investigation or surveillance services.

The Tax Office had recently issued more than 16,000 penalties to businesses which failed to lodge previous TPARs with the average penalty about $1,110.

The ATO also said that failure to meet the deadline could be seen as a “red flag and prompt closer scrutiny”.

The TPAR is just one weapon in the ATO’s arsenal helping expose missing income and keeping things fair for businesses doing the right thing.

Steps to work out if you need to lodge

Step 1: calculate your total payments received from contractors for each relevant service.

Add up all payments your business received for each relevant TPRS service during the financial year. Include payments received when employees, contractors or sub-contractors performed services on your behalf.

Step 2: calculate your current or projected business income

If you have been operating your business for:

• the full financial year: use your current business income for the year

• less than 12 months of the financial year: use your projected business income. Do this by working out what your business income will be for the next full financial year.

Step 3: calculate what per cent of your business income is from a relevant service

Calculate this percentage by using the following formula for each financial year:

Total payments received for a relevant service ÷ current or projected business income x 100 = %

You must lodge a TPAR if:

• 10% or more of your business income for the financial year is from a relevant service, and

• you made payments to contractors for a relevant service during the year.

If you need to lodge a TPAR, report the total contractor payments made to each contractor for the relevant service provided on your behalf.

Read our article on how to avoid ATO penalties.

How a registered trade mark can grow your sales and your business

Ensure your business plan contains all the different components including organisational, marketing, operational, financial and risk analysis. If you don’t know where to start contact us today.

Ensure your business plan contains all the different components including organisational, marketing, operational, financial and risk analysis. If you don’t know where to start contact us today.

Did you know that in 2022 almost 30% of all Australian businesses with a registered trade mark were in Victoria? Your brand is often the first thing your customers see when interacting with your business, and by registering a trade mark for it, you have peace of mind that your brand is legally protected.

In addition, a business with a registered trade mark is 13% more likely to achieve high turnover growth, according to a study by IP Australia.

Despite the positive data, less than 4% of Australian small businesses have a registered trade mark.

What is a trade mark?

A registered trade mark legally protects your business’s unique brand, products or services, and helps customers distinguish your products or services in the market.

Those without a registered trade mark may be missing out on these potential benefits:

- after filing for an intellectual property (IP) right, such as a registered trade mark, small to medium enterprises (SMEs) are 16% more likely to experience high employment growth compared to businesses with no recent IP filings, according to research by IP Australia

- for businesses launching products, each additional registered trade mark is linked to an 8% revenue increase per employee

- applying for a trade mark is linked to an increase in start-up valuation

- SMEs that own IP rights on average employ 3.5 times as many people as their peers with no IP rights and pay a higher median wage.

But what about the businesses that don’t check their branding? Checking the availability of your brand name or logo can be important to avoid infringing a competitor’s registered trade mark. By not checking, businesses can run the risk of needing to rebrand and may face litigation, and the associated costs. Check out the numbers below.

Case Study – Fat Duck vs Heston Blumenthal

The Fat Duck restaurant opened in Sydney in 2011. Shortly after opening, the restaurant was required to relinquish their name and rebrand.

This rebranding was a result of celebrity chef Heston Blumenthal filing an application for trade mark protection. Intending to reserve and protect the name for his chain of fine dining restaurants, Heston’s company filed a claim in the Federal Court of Australia and won, having filed all the requirements for the trade mark rights.

The Fat Duck restaurant was required to rebrand their business, demonstrating that if you haven’t protected your name or logo against competitors, you may run the risk of losing the rights to it.

Case Study – SEO Shark

SEO Shark is a digital marketing agency that specialises in search engine optimisation (SEO).

SEO Shark is a digital marketing agency that specialises in search engine optimisation (SEO).

In conversation with IP Australia, SEO Shark® explained that “as competition grew, we knew in order to protect and differentiate the brand from other businesses we needed to trade mark the name. The SEO Shark trade mark is our identity, the way we show who we are to customers and this is something we don’t want another business to replicate. We now have the name and logo of SEO Shark registered, meaning we can prevent other businesses in Australia using our trade marks.”

Their advice for other businesses looking to protect their brand is to understand the time and costs involved in applying for a trade mark. They may not be as much as you think! The cost of a trade mark is often assumed to be beyond the budget of a small business, but in total, the cost of protecting SEO Shark® was about $600 for ten years’ protection.

Case Study – Tutu by You

Tutu by You was launched in 2020 by business partners and cousins, Steph Young and Emily Murray. They wanted to create a brand for kids, and something that would bring much joy and happiness to the world. Their strategy for IP protection was to protect what they could, with an emphasis on making sure they used the right type of protection.

Emily told IP Australia, “Protecting our IP is so important because it’s everything, right? We’ve worked so hard on this. We’ve only launched six months ago, but we’ve been working on this for two and a half years. There were moments where we thought, ‘Do we really need to spend that money to get that protected? Is anyone going to care about us? Are they really going to try and rip us off?’ You just don’t know. It’s a risk. You’ve got to take it.”

Emily told IP Australia, “Protecting our IP is so important because it’s everything, right? We’ve worked so hard on this. We’ve only launched six months ago, but we’ve been working on this for two and a half years. There were moments where we thought, ‘Do we really need to spend that money to get that protected? Is anyone going to care about us? Are they really going to try and rip us off?’ You just don’t know. It’s a risk. You’ve got to take it.”

Tutu by You wanted to protect their business name using a trade mark, and their unique ‘sparkle band’ using a design right. They now feel confident in taking their products to market across all platforms because of their IP protection.

To read the full case study visit IP Australia’s website.

How can you check and register a trade mark?

The new, free pilot TM Checker tool makes it easier for small businesses to check if a trade mark is available. An initial check only takes a few minutes, then you can apply to register for a trade mark using the tool for as little as $330.

Registering your trade mark gives you:

Registering your trade mark gives you:

- a business asset: the more successful your business becomes, the more valuable your trade mark becomes.

- the legal right to place the ® symbol next to your trade mark

- exclusive rights to use your trade mark in Australia

- the ability to legally deter others from using your trade mark

- the ability to sell your trade mark, or license it for others to use.

Small business owner Deborah had this to say about TM Checker:

“We would recommend this for the other small businesses as the cost of losing your brand or name is very high. It is also very costly to dispute a legal challenge and to rebrand, redefine or re-leverage any products or market share.”

Remember that a registered trade mark can be used to protect anything that identifies your business such as a brand name, logo, distinctive phrase, letter, number, colour, sound, smell, shape, picture, movement, aspect of packaging or a combination of these. Contact us today and we can refer you to one of our business partners in this area.

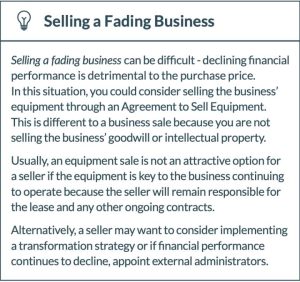

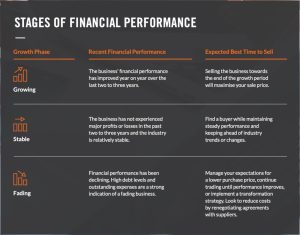

When to Sell Your Business

Timing is crucial when it comes to selling your business. Market conditions and industry performance at the time of sale will have an impact on the price you can get for your business. Determining the best time to sell is an art rather than a science, but there are two important factors to consider for every sale:

- The recent financial performance of your business.

- Market trends for your industry.

FINANCIAL PERFORMANCE

A business’ financial performance is a major factor in determining the purchase price. The goal of the seller should be to obtain the best possible price for their business. The price will differ depending on many factors, including whether the growth of the business is increasing, fading or stable.

HOW TO CONDUCT MARKET RESEARCH

There’s rarely a ‘right time’ to sell your business.

And determining the ‘right price’ is next to impossible. But some research can be valuable when it comes to choosing when and how to sell your business.

Your market research should focus on two areas: (i) future demand for your product or services; and (ii) demand for your business.

1 Future Demand for Your Product or Services

A business’ value should always be measured by its future cash flows, which are partly determined by the future demand for your product or services.

A business’ value should always be measured by its future cash flows, which are partly determined by the future demand for your product or services.

Economic and industry trends can have large, long-term effects on sales and profit. For example, when consumer confidence is high, customers are more likely to spend disposable income on goods and services, like clothes and entertainment. The increased demand for products and services could mean business owners can charge higher prices.

To find economic and industry information, start by reading the economics section of the Australian Financial Review. To go deeper, check out the economic commentary from the Reserve Bank of Australia. Finally, the Australian Bureau of Statistics is a trove of industry-specific data.

2 Demand for Your Business

Just like the housing market, the market for businesses is cyclical. If there is more demand than supply for businesses like yours, you can request a higher price.

For example, if more people want to purchase a cafe than there are cafes available for purchase, then owners of cafes can charge a higher price when selling their business.

Determining the relative levels of demand and supply for businesses can be a challenge. The best way is to ask a business broker. Brokers are experts who spend their days scanning the market for businesses — gauging demand and assessing supply. Speak to three or four brokers from different organisations to make sure you get a balanced view of market conditions.

Finally, spend a few weeks scanning the listings for businesses similar to yours that are on the market. You will start to get a sense for the value of your business by asking, at what price are they selling? and how long do they take to sell?

DRAFTING AN EXIT PLAN

Selling a business that is underprepared for a sale can negatively impact the buyer’s perception of your business, and the purchase price. Before speaking with potential buyers, you should plan for the sale by drafting an exit plan setting out the steps you need to take to ensure you can sell your business for its maximum value.

The exit plan should deal with:

Completing the sale of a Business

MARKET TRENDS

In addition to the financial performance of your business, market trends can affect when it’s a good time to sell.

In addition to the financial performance of your business, market trends can affect when it’s a good time to sell.

Selling a business involves several steps, moving parts and legal documents. Once you negotiate and exchange a business sale agreement with the other party, parties must transition to the completion process. This broadly involves the buyer and seller’s lawyers working together (and with their respective clients) to fulfil a number of obligations. Once all parties satisfy these obligations, the sale will be complete. Completion can be a stressful and overwhelming process, so it is useful to prepare a complete checklist to keep track of progress. This article discusses the key stages and documents common to most business sale transactions.

Pre-Completion Steps

Before the parties can complete the sale, there are several steps they must take to get ready for the big day (known as completion day). Each of the buyer and seller’s lawyers must review the business sale agreement carefully to ensure their respective clients satisfy these steps. Indeed, many of them can take time and may delay the sale if left to the last minute.

The table below sets out some common pre-completion steps and the documents required to satisfy them.

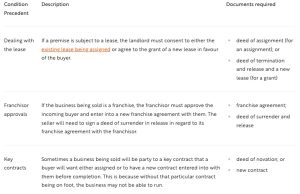

Conditions Precedent

Throughout the business sale agreement, there are several conditions that must be satisfied before the completion date. These are known as conditions precedent.

Throughout the business sale agreement, there are several conditions that must be satisfied before the completion date. These are known as conditions precedent.

It is usually a term of the sale agreement that if these conditions are not satisfied by the relevant party (or waived by the party which has the benefit of them), the other party can walk away from the sale. In the case of the buyer, they can potentially have their deposit refunded.

The table below sets out some common conditions precedent in a business sale and the documents required to satisfy them.

Completion Day

On the completion date, both parties must work together to fulfil their respective obligations. Completion can differ greatly between transactions depending on what the business is and what assets are being sold. However, there are some obligations that are usually present in each business sale. Once the completion obligations have been fulfilled by both parties, the sale has been completed and the buyer is now the legal owner of the business.

The table below sets out some common completion obligations in a business sale.

Post-Completion Obligations

Post-Completion Obligations

Sometimes there are post-completion obligations for the seller. These often include training the buyer on the business processes for a certain period of time. It can also include an agreement to be on call for a certain period of time for technical questions and assistance following the sale. The seller will usually have restraint obligations to comply with a certain period of time post-completion.

Key Takeaways

Completion can be a daunting and stressful process, as there can be a number of steps and obligations which both parties must adhere to ensure a smooth end to the transaction. Completion involves a three-step process: pre-completion, day of completion, and post-completion. All of these steps involve different documents and requirements.

Completion can be a daunting and stressful process, as there can be a number of steps and obligations which both parties must adhere to ensure a smooth end to the transaction. Completion involves a three-step process: pre-completion, day of completion, and post-completion. All of these steps involve different documents and requirements.

Of particular importance are the conditions precedent in the pre-completion stage, as if these are not fulfilled or waived, the other party will usually have the right to terminate the agreement and walk away from the sale. Likewise, in the case of the buyer, they can potentially have their deposit refunded. It is a good idea to keep a completion checklist handy so all parties can keep track of where things are at with completion.

Business Start Up Corner – Funding Your New Business

Business Start Up Corner – Funding Your New Business

Raising money for your new business venture is often the biggest challenge for a start-up entrepreneur. The truth is, it’s not that easy for an established business to gain funding either!

As a start-up business, your chances of securing finance are improved if you have industry experience, good references and support from a great mentor. However, you also need to create and document the best business plan ever!

Business Plan & Cash Flow Budget

While the main reason most people prepare a business plan is to raise finance, your business plan should also prove the viability of your business venture. Included in the business plan is a cash flow budget for the first year of trading and a positive cash flow is an absolute necessity if your business is to succeed. Positive cash flow doesn’t just happen, it needs to be planned.

While the main reason most people prepare a business plan is to raise finance, your business plan should also prove the viability of your business venture. Included in the business plan is a cash flow budget for the first year of trading and a positive cash flow is an absolute necessity if your business is to succeed. Positive cash flow doesn’t just happen, it needs to be planned.

That’s why we strongly recommend the preparation of a 12-month cash flow budget before you start your business. In fact, any business that fails to accurately forecast its cash flow in the first 12 months is on a collision course because, without realistic cash flow projections, management is unable to identify future cash shortages.

The cash flow budget is based on a number of assumptions regarding the expected future performance of the business. The assumptions must be realistic and supported by research, available data plus known facts such as rentals or forward contracts. The information in your cash flow budget is designed to:

- Forecast your likely cash position at the end of each month;

- Identify any fluctuations that may lead to potential cash shortages;

- Plan for your taxation payments;

- Plan for any major capital expenditure; and

- Provide prospective lenders with key financial information.

Of course, positive cash flow alone is not enough. The business must be returning a profit and the long-term trend for both must be positive.

To obtain funding within the banking system you should:

To obtain funding within the banking system you should:

- Practice your presentation skills;

- Present credible references;

- Produce an outstanding business plan; and

- Keep your credit history clean.

Funding outside the bank system:

- Investigate Government or other Grants;

- Angel investors;

- Crowdfunding; or

- Seed funding (where an investor purchases part of a business)

IMPORTANT DISCLAIMER: This document contains general advice only and is prepared without taking into account your particular objectives, financial circumstances and needs. The information provided is not a substitute for legal, tax and financial product advice. Before making any decision based on this information, you should speak to a licensed financial advisor who should assess its relevance to your individual circumstances. While the firm believes the information is accurate, no warranty is given as to its accuracy and persons who rely on this information do so at their own risk. The information provided in this bulletin is not considered financial product advice for the purposes of the Corporations Act 2001.